- Call us: +91 996 640 1975

- E-Mail: info@pmry.in

International Taxation

Our Clients

Payroll Management

Payroll Management Accounts Outsourcing

Accounts Outsourcing Company LLP Formation

Company LLP Formation FEMA & RBI COMPLIANCE

FEMA & RBI COMPLIANCE Transfer Pricing Report

Transfer Pricing Report Preparation of Business Plan

Preparation of Business Plan Foreign Company

Foreign Company Goods and Services Tax (GST)

Goods and Services Tax (GST) Entry Strategy For India

Entry Strategy For India

Our Services

International Taxation As per The Income Tax Act, 1961.

All the international aspects of income tax law of a particular nation is generally referred as international taxation. International Taxation in India involves Transfer Pricing, Master File, CBC Reporting, DTAA, GAAR, BEPS etc.

What is Transfer Pricing?

- In simple terms, Transfer Pricing refers to the Price charged between two or more entities of an MNC (Associated Enterprises) operating in different countries for goods, services, or use of property (including intangible property).

Is Transfer Pricing Report mandatory?

- Transfer Pricing Report is to be maintained mandatorily if the aggregate value of international transactions during the Financial Year exceeds 1 Crore.

- In case of Specified Domestic Transactions aggregate value of transactions during the Financial Year should exceed 2 Crores.

About New amendment Section 92

Master File and Country by Country Reporting

Base Erosion Profit Shifting (BEPS):

Meaning

- Base erosion and profit shifting (BEPS) refers to tax avoidance strategies that exploit gaps and mismatches in tax rules to artificially shift profits to low or no-tax locations. Under the inclusive framework, over 100 countries and jurisdictions are collaborating to implement the BEPS measures and tackle BEPS.

- Usually, a company has to pay tax for its profit or income. The profit is the tax base for the government as tax is imposed as a percentage of the profit. Once profit is shifted to other countries or to tax havens, the tax base is eroded and there is no tax payment by the company in the concerned country.

- Organization for Economic Cooperation and Development (OECD)’s Base Erosion and Profit Shifting (BEPS) initiative seeks to close gaps in international taxation for companies that allegedly avoid taxation or reduce tax burden in their home country by engaging in tax evasion (moving operations) or by migrating intangibles to lower tax jurisdictions.

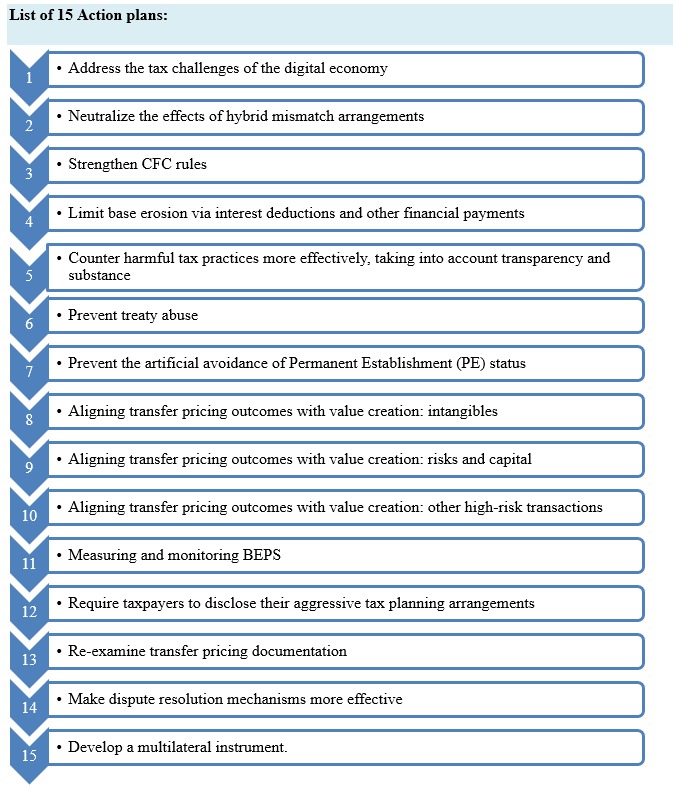

- OECD has issued 15 Action Plans to address the main areas where they feel companies have been most aggressively accomplishing this shifting of profit — addressing the digital economy, treaty abuse, transfer pricing documentation, and more. BEPS Action Plan 13, in particular, aims to transform transfer pricing documentation, forcing multinational corporations to reconsider how transfer pricing details are reported to local tax authorities as well as worldwide with country-by- country reporting

BEPS Action Plan:

The BEPS Package provides 15 Actions that equip governments with the domestic and international instruments needed to tackle BEPS. Countries now have the tools to ensure that profits are taxed where economic activities generating the profits are performed and where value is created. These tools also give businesses greater certainty by reducing disputes over the application of international tax rules and standardizing compliance requirements.

List of 15 Action plans:

Impact on Indian Tax Law:

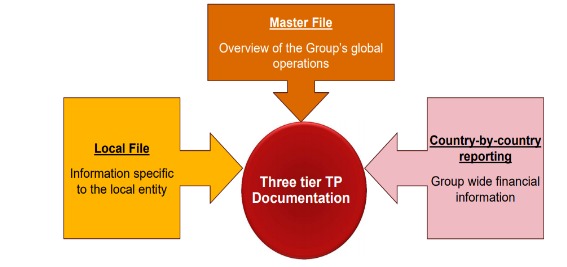

- Indian Income tax law has come up with a three-tier documentation structure, by following the recommendations of Organization for Economic Cooperation and Development (OECD) under Action 13 of the Base Erosion and Profit Shifting (BEPS) project.

- The Finance Act, 2016 introduced Section 286 to the Income-tax Act, 1961 providing for furnishing of Country by Country (CBC) report in respect of an international group. Section 92D of the Act which contained provisions for preparing TP documentation was also amended to provide for furnishing of Master File.

- Rules 10DA and 10DB have been inserted in the Income-tax Rules, 1962 (the Rules). Forms 3CEAA, 3CEAB, 3CEAC, 3CEAD and 3CEAE have also been notified under the above rules.

Rule 10DA (Section 92D)

Lays down the time lines in relation to master information and file is required to be 3CEAB. theseholds for applicability, requirements and procedures File. The relevant intimation related to Master filed in Forms 3CEAA and

Rule 10DB (Section 286)

Lays down the requisite details and procedures for CBC report filing. The relevant information and intimations is required to be filed in Forms 3CEAC, 3CEAD and 3CEAE.

Master File (MF) – Rule 10DA

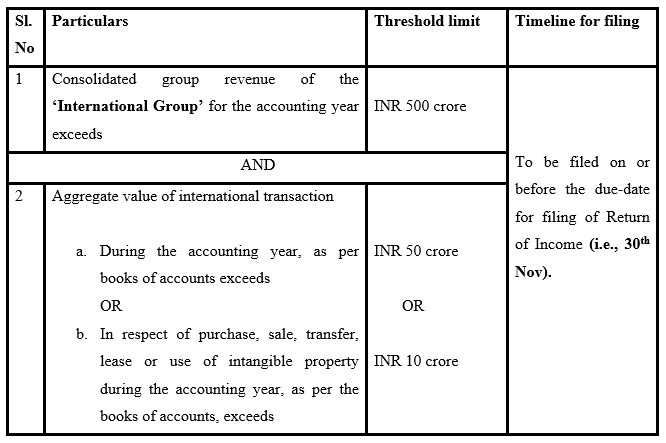

As per rule 10DA, if the international group satisfies the following both conditions, a detailed master file should be filed by the Constituent entity resident in India:

Country by Country Report – Rule 10DB

What are the Databases considered for Data of Comparable Companies for TP Documentation?

- ProwessIQ and Capitaline ICAI Databases are the databases available to compare the results of a company with other companies to determine ALP.

Income Tax Compliance

- As per Income Tax Act companies who are required to file TP reports has to file FORM 3CEB to the Tax department duly certified by a Chartered Accountant.

- Contents of Transfer Pricing Report:

» Description of the International Transactions with Associated Entities

» FAR Analysis of Tested party (Functions, Assets & Risks)

» Computation of Arm’s Length Price

Why consulting from us?

- Planning, Review & Evaluation of Transfer Pricing Mechanism.

- Adherences and Compliance of Transfer Pricing Regulations and Provisions as according with present Legislations.

- Representation before the competent authorities.

- Expert tax planning with a flexible approach on implementation of methodologies of transfer pricing.

- Consultancy services on Potential threats interrelated with the existing legislation and the policies of the organization to avoid Taxation & legal Consequences.

We provide full strength professional services on activities relating to Transfer Pricing as according to ALP pronounced by the prescribed authorities in this respect. We assist you in the following aspects of Transfer Pricing :